College Planing & 529 Plan

Funding College Education

1

IUL has unique features that can make it a match for saving for college education .

While the death benefit of a life insurance policy helps to ensure that families can meet the financial obligations in the event of the death of a loved one, IUL has the potential to provide additional benefits as well. Premiums paid towards a IUL policy can, in essence, serve dual purposes. The same policy that protects loved ones may also build accumulation value that can be used for a variety of needs, including funding education.

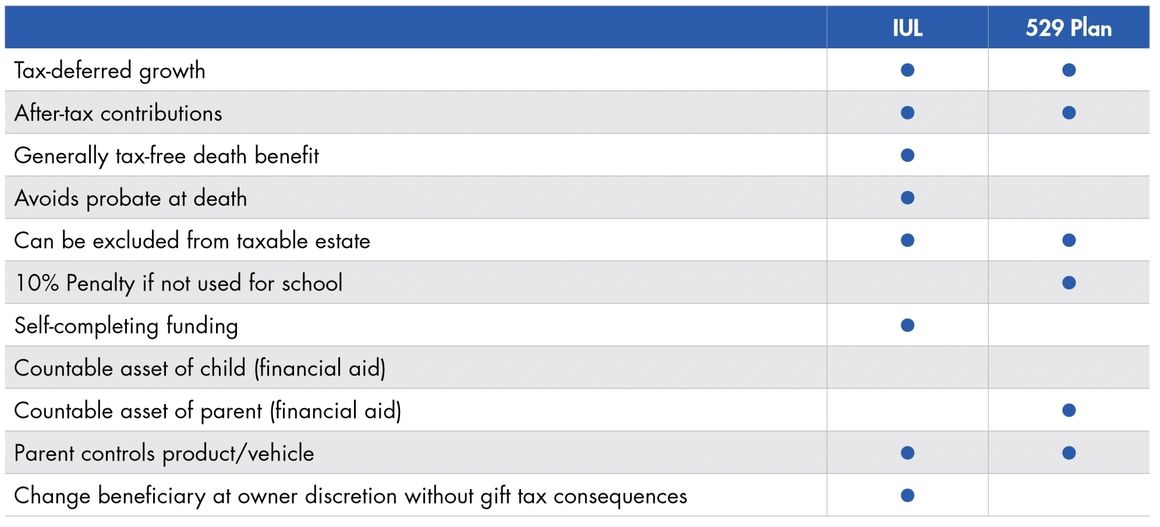

As tuition prices continue to rise, families must plan to put away more money for their children’s and grandchildren’s future education needs. Some fund this need using mutual funds, CDs, 529 Education Savings Plans, or permanent life insurance that builds accumulation value.

An advantage of life insurance not enjoyed by any other funding vehicle is that the generally tax-free death benefit provides self-completing funding if the insured dies prematurely, guaranteeing that the funds will be there for your child or grandchild to complete school. In other plans, such as 529 Plans, if the plan owner dies early, the plan may not be appropriately funded causing a shortage when it is time to pay for college. Additionally, the accumulation value in a permanent life insurance policy is not currently a countable asset when applying for federal financial aid.

IUL could be a great fit for families that need life insurance protection along with a potential solution to fund education. Policy loans can be used to gain access to the policy’s accumulation value, which could then be used to fund education 2. The idea is to fund a IUL policy early with a large enough face amount to provide a good death benefit, accumulation value for policy loans, or high surrender value for the costlier things in life —like funding your children or grandchildren’s educations.

While the death benefit of a life insurance policy helps to ensure that families can meet the financial obligations in the event of the death of a loved one, IUL has the potential to provide additional benefits as well. Premiums paid towards a IUL policy can, in essence, serve dual purposes. The same policy that protects loved ones may also build accumulation value that can be used for a variety of needs, including funding education.

As tuition prices continue to rise, families must plan to put away more money for their children’s and grandchildren’s future education needs. Some fund this need using mutual funds, CDs, 529 Education Savings Plans, or permanent life insurance that builds accumulation value.

An advantage of life insurance not enjoyed by any other funding vehicle is that the generally tax-free death benefit provides self-completing funding if the insured dies prematurely, guaranteeing that the funds will be there for your child or grandchild to complete school. In other plans, such as 529 Plans, if the plan owner dies early, the plan may not be appropriately funded causing a shortage when it is time to pay for college. Additionally, the accumulation value in a permanent life insurance policy is not currently a countable asset when applying for federal financial aid.

IUL could be a great fit for families that need life insurance protection along with a potential solution to fund education. Policy loans can be used to gain access to the policy’s accumulation value, which could then be used to fund education 2. The idea is to fund a IUL policy early with a large enough face amount to provide a good death benefit, accumulation value for policy loans, or high surrender value for the costlier things in life —like funding your children or grandchildren’s educations.

IUL vs. 529 Education Savings Plans

Case Study

1

THE CHALLENGE

Darrell and Christine, age 35, felt they needed life insurance protection for Christine and their two young children in the event something happened to Darrell, who was the primary means of support. The couple also wanted to have the option to help their children pay for their education.

THE SOLUTION

They talked to their financial adviser and determined a $500,000 IUL policy could help cover several of the risks faced by their family. In the event that something were to happen to Darrell, they would have protection for the family that could cover education costs for the children, pay off the family home, provide Christine funds to run the home, or provide some funds to put away for her retirement. While their children are growing up, the accumulation value in the policy would continue to grow. When it is time for their children to attend college, Christine and Darrell could choose to take policy loans from their accumulation value to pay for their education expenses. Lastly, their adviser added that the policy also included Accelerated Benefit Riders 1 for Critical, Chronic, and Terminal illnesses. In the event that Darrell was diagnosed with a qualifying illness, he may be able to accelerate all or part of the death benefit and receive an unrestricted cash benefit. This could give Darrell and Christine the option to assist with their children’s education even in the event that Darrell suffered an illness that made him unable to work.

CONTACT US

College Planning